Global Digital Health Market Size and Trends By Revenue, Region, and Segment Forecasts (2024 – 2029)

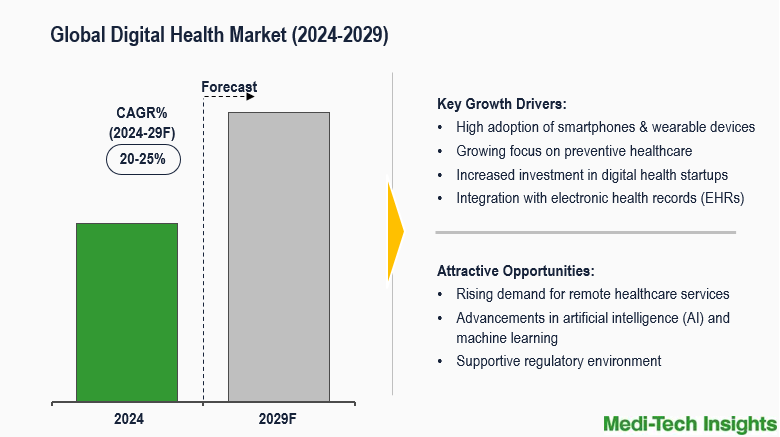

The global digital health market is set to witness a significant growth rate of 20-25% in the next 5 years. increasing adoption of smartphones and wearable devices, rising demand for remote healthcare services, advancements in artificial intelligence (AI) and machine learning, growing focus on preventive healthcare, increased investment in digital health startups, supportive regulatory environment, and integration with electronic health records (EHRs) are some of the key factors driving the digital health market. To learn more about the research report, download a sample report.

Digital health refers to the use of digital technologies, such as mobile health apps, wearable devices, telemedicine platforms, and artificial intelligence, to enhance healthcare delivery and improve patient outcomes. It encompasses a wide range of tools and systems that enable real-time monitoring, data collection, and personalized care. By leveraging innovations in connectivity, data analytics, and automation, digital health promotes preventive care, empowers individuals to manage their health, and enables healthcare providers to offer remote, accessible, and efficient services. This approach aims to make healthcare more patient-centric, cost-effective, and sustainable.

Increasing adoption of smartphones and wearable devices to propel market demand

As smartphones and wearables become more advanced, they are transforming how individuals manage their health and how healthcare is delivered. Globally, smartphone usage has reached unprecedented levels. According to the GSMA, there were around 5.3 billion smartphone users in 2022, which equates to about 67% of the global population. This widespread adoption creates a solid foundation for mobile health (mHealth) applications, which provide users with tools to track their physical activity, nutrition, sleep patterns, and overall well-being. Fitness and wellness apps, such as MyFitnessPal, Sleep Cycle, and Strava, are commonly used for managing personal health goals. Wearable devices are also gaining popularity due to their ability to monitor vital signs and health metrics in real-time. Devices like the Apple Watch, Fitbit, and Garmin provide users with real-time information on heart rate, blood oxygen levels, physical activity, and even ECG monitoring. Apple’s WatchOS 7 introduced the ability to monitor sleep and detect potential health issues, enhancing its role as a personal health management tool.

In healthcare settings, wearables and smartphones are becoming crucial for remote monitoring of patients with chronic conditions. For example, diabetes patients can now use glucose-monitoring devices like the Dexcom G6, which continuously tracks blood sugar levels and sends real-time alerts to the patient’s smartphone. This empowers patients to manage their condition proactively, while healthcare providers can intervene when necessary. The increasing adoption of these technologies is revolutionizing the digital health market, offering more accessible and personalized care options, and driving further investment and innovation in the field.

Furthermore, smartphones and wearables offer several benefits in digital health by enabling real-time health monitoring and providing immediate feedback. They help patients take control of their health by tracking vital signs and encouraging better management of conditions like diabetes and heart disease. Remote monitoring reduces the need for hospital visits, making healthcare more accessible and cost-effective. These devices can also detect early signs of health problems, allowing for timely intervention. Additionally, they provide personalized health insights and integrate seamlessly with electronic health records, helping doctors make better decisions and improving overall patient care.

To learn more about this report, download the PDF brochure

Continuous innovation in digital health driving the market growth

Technological advancements in digital health are revolutionizing the healthcare industry, driving significant market growth by improving patient care and streamlining healthcare delivery. Innovations such as artificial intelligence (AI), machine learning, wearable devices, and telemedicine platforms are transforming how health data is collected, analyzed, and utilized. These technologies enable real-time monitoring, early disease detection, and personalized treatment plans, empowering both patients and healthcare providers. Some of the technological advancements are listed below-

- In January 2024, Withings introduced the BeamO at CES 2024, a new 4-in-1 device that integrates an electrocardiogram (ECG), oximeter, stethoscope, and thermometer, enabling users to monitor heart and lung health, as well as body temperature from home

- In September 2023, Apple unveiled the Apple Watch Series 9, featuring enhanced health monitoring capabilities, including improved sensors for better accuracy in tracking metrics like heart rate, blood oxygen levels, and new health-focused apps. The new watch is equipped with a new S9 SiP that increases performance and capabilities featuring double tap gesture, brighter display, and faster on-device Siri

- In August 2021, Fitbit introduced the Charge 5, a fitness-tracking wearable which includes advanced health features such as ECG monitoring, stress management, and improved sleep tracking, aimed at offering comprehensive health insights

As digital health solutions become more sophisticated and accessible, they are playing a crucial role in reducing healthcare costs, enhancing patient outcomes, and addressing the growing demand for remote and preventive care. Such advancements tend to provide competitive edge to manufacturers and therefore, major players are continuously focusing on investing in research activities for new product development and expanding their geographic reach to strengthen their positions in this high growth market.

Favorable funding environment fuels the growth of the digital health market

Recent funding in digital health has significantly driven market growth by spurring innovation and advancing technology across various domains, including telehealth, mHealth, and digital therapeutics. Investment enables companies to expand their geographic reach, enhance product development, and improve accessibility, which boosts adoption rates. Additionally, funding supports the integration of advanced technologies like AI and data analytics, making solutions more effective and attractive. These factors collectively increase consumer confidence and demand, contributing to a broader market base and accelerated growth in the digital health sector.

In recent years, the digital health market has witnessed an increase in funding for startups that helps in driving innovation, expanding capabilities, and improving the accessibility and effectiveness of healthcare solutions across various domains. Some of the related developments are listed below-

- In July 2024, K Health, a telehealth company providing AI-driven consultations and personalized health insights, has secured a funding of $ 50 million in an equity funding round to expand its virtual care services. The company has earlier raised $60 million in a Series D funding round in August 2023

- In October 2023, HealthEC has secured additional financing from HLM Venture Partners and Labcorp Venture Fund. This funding is expected to support the expansion of their AI-enabled Population Health Management platform and growth in value-based and behavioral health management areas

- In July 2022, Elation Health secured $50 million in Series D funding, co-led by Generation Investment Management and Ascension Ventures, boosting its total to $108.5 million. The funds are aimed at enhancing its cloud-hosted, API-enabled electronic health record (EHR) system, expanding features and market reach to support value-based primary care

- In June 2022, WEMA Health, a digital health startup, launched its services in the UAE after raising $3.50 million in a seed funding round led by Dawn Health, Europe’s digital health company. The firm provide a virtual obesity programme to help its members lose up to 20% of their body weight by deploying in-house experts

To learn more about this report, download the PDF brochure

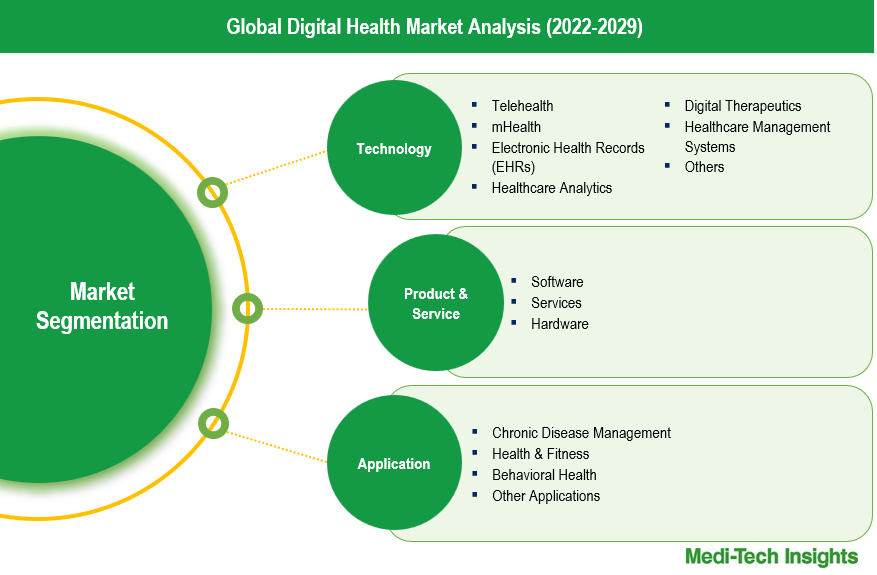

Technology Segment Outlook

Digital health technologies are revolutionizing healthcare by enhancing accessibility, improving patient outcomes, and streamlining operations. Based on technology the digital health market is segmented into telehealth, mHealth, electronic health records (EHRs), healthcare analytics, digital therapeutics, healthcare management systems, and others. The telehealth segment has seen rapid growth, especially in response to the COVID-19 pandemic, which accelerated the adoption of remote consultations and services, is driven by increased demand for remote care and advancements in communication technologies. The EHR segment also holds a significant market share in the digital health market due to its widespread adoption across healthcare systems, ongoing digital transformation and regulatory requirements, and its ability to improve data management and interoperability. Furthermore, the mHealth market is experiencing significant growth due to several key factors that include widespread smartphone adoption, increased health awareness, advancements in technology, rising chronic diseases, and integration with other technologies.

Regional Outlook: North America expected to hold a major share in the digital health market

From a geographical perspective, North America remains a key market for digital health, supported by combination of technological advancements, increasing healthcare demands, and supportive regulatory environments. The digital health market in North America is experiencing significant growth, driven by high adoption rates, favorable regulatory and funding environment, increased focus on patient-centric care, strong research and development capabilities, and robust healthcare infrastructure. The region, particularly the US, has been at the forefront of innovation in healthcare technologies, including the development and adoption of digital health. Its regulatory frameworks, substantial funding, and extensive integration of digital health technologies shape the market, setting trends and standards that influence both regional and global developments.

The digital health market faces several challenges, including data privacy and security concerns, interoperability issues, regulatory hurdles, high implementation costs, and resistance from patients and providers. Ensuring the protection of sensitive information, integrating new technologies with existing systems, and navigating complex regulations can hinder growth. Additionally, the high costs of adoption and reluctance to change can impact market expansion. Despite these obstacles, the digital health market is expected to experience significant growth. Key drivers include technological advancements, rising consumer demand for personalized and convenient care, supportive government policies, and a shift towards value-based care. Innovations in telehealth, mHealth, and digital therapeutics, coupled with increasing investments and collaborations, are likely to address these challenges and drive the market growth.

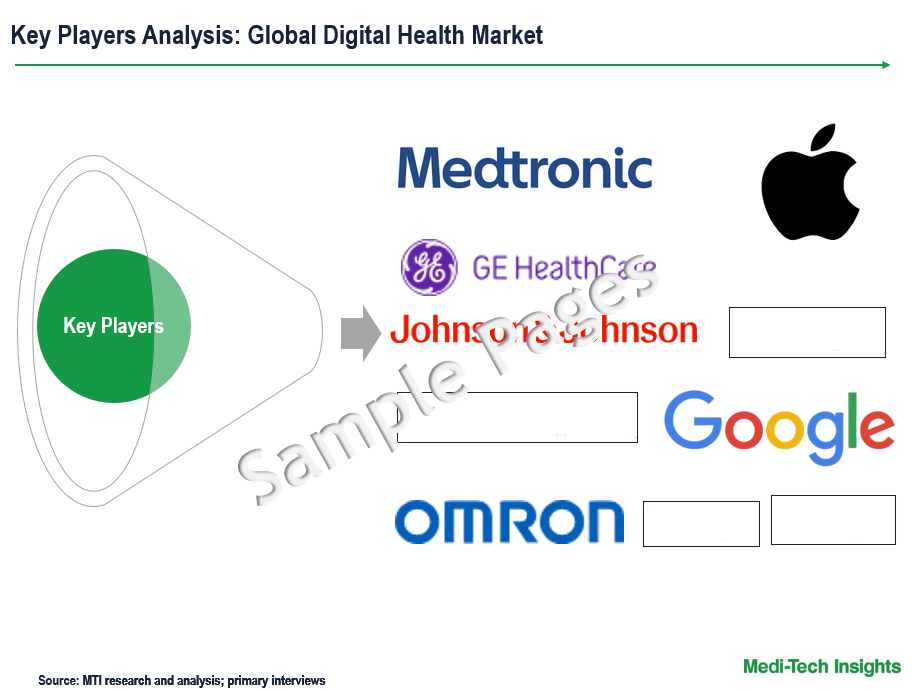

Competitive Landscape Analysis

The global digital health market is marked by the presence of established and emerging market players such as Koninklijke Philips N.V. (Netherlands); Medtronic plc (Ireland); GE HealthCare (US); OMRON Corporation (Japan); Google, Inc. (US); Johnson & Johnson Services, Inc. (US); Siemens Healthineers AG (Germany); Apple Inc. (US); Veradigm LLC (US); athenahealth (US); among others. Some of the key strategies adopted by market players include product innovation and development, strategic partnerships and collaborations, mergers and acquisitions, and geographic expansion.

Get a sample report for competitive landscape analysis

Digital Health Market Scope

|

Report Scope |

Details |

|

Base Year Considered |

2023 |

|

Historical Data |

2022 - 2023 |

|

Forecast Period |

2024 - 2029 |

|

Growth Rate |

CAGR 20-25% |

|

Segment Scope |

Technology, Application, End User |

|

Regional Scope |

|

|

Key Companies Mapped |

Koninklijke Philips N.V.; Medtronic plc; GE HealthCare; OMRON Corporation; Google, Inc.; Johnson & Johnson Services, Inc.; Siemens Healthineers AG; Apple Inc.; Veradigm LLC; athenahealth; among others |

|

Report Highlights |

Market Size & Forecast, Growth Drivers & Restraints, Trends, Competitive Analysis |

Key Strategic Questions Addressed

- What is the market size & forecast of the digital health market?

- What are historical, present, and forecasted market shares and growth rates of various segments and sub-segments of the digital health market?

- What are the key trends defining the market?

- What are the major factors impacting the market?

- What are the opportunities prevailing in the market?

- Which region has the highest share in the global market? Which region is expected to witness the highest growth rate in the next 5 years?

- Who are the major players operating in the market?

- What are the key strategies adopted by players?

- Introduction

- Introduction

- Market Scope

- Market Definition

- Segments Covered

- Regional Segmentation

- Research Timeframe

- Currency Considered

- Study Limitations

- Stakeholders

- List of Abbreviations

- Key Conferences and Events (2023-2024)

- Research Methodology

- Secondary Research

- Primary Research

- Market Estimation

- Bottom-Up Approach

- Top-Down Approach

- Market Forecasting

- Executive Summary

- Digital Health Market Snapshot (2023-2029)

- Segment Overview

- Regional Snapshot

- Competitive Insights

- Market Overview

- Market Dynamics

- Drivers

- High adoption of smartphones & wearable devices

- Growing focus on preventive healthcare

- Increased investment in digital health startups

- Integration with electronic health records (EHRs)

- Continuous innovation in digital health

- Restraints

- Data privacy and security concerns

- High implementation costs

- Regulatory hurdles

- Opportunities

- Rising demand for remote healthcare services

- Advancements in artificial intelligence (AI) and machine learning

- Supportive regulatory environment

- Key Market Trends

- Drivers

- Unmet Market Needs

- Industry Speaks

- Market Dynamics

- Global Digital Health Market Size & Forecast (2022-2029), By Product & Service, & Service, USD Million

- Introduction

- Software

- Services

- Hardware

- Global Digital Health Market Size & Forecast (2022-2029), By Technology, USD Million

- Introduction

- Telehealth

- mHealth

- Electronic Health Records (EHRs)

- Healthcare Analytics

- Digital Therapeutics

- Healthcare Management Systems

- Others

- Global Digital Health Market Size & Forecast (2022-2029), By Application, USD Million

- Introduction

- Chronic Disease Management

- Health & Fitness

- Behavioral Health

- Other Applications

- Global Digital Health Market Size & Forecast (2022-2029), By End User, USD Million

- Introduction

- Patients

- Providers

- Payers

- Other End Users

- Global Digital Health Market Size & Forecast (2022-2029), By Region, USD Million

- Introduction

- North America Digital Health Market Size & Forecast (2022-2029), By Country, USD Million

- US

- Market Size & Forecast, By Product & Service, (USD Million)

- Market Size & Forecast, By Technology (USD Million)

- Market Size & Forecast, By Application (USD Million)

- Market Size & Forecast, By End User (USD Million)

- Canada

- Market Size & Forecast, By Product & Service, (USD Million)

- Market Size & Forecast, By Technology (USD Million)

- Market Size & Forecast, By Application (USD Million)

- Market Size & Forecast, By End User (USD Million)

- Europe Digital Health Market Size & Forecast (2022-2029), By Country, USD Million

- UK

- Market Size & Forecast, By Product & Service, (USD Million)

- Market Size & Forecast, By Technology (USD Million)

- Market Size & Forecast, By Application (USD Million)

- Market Size & Forecast, By End User (USD Million)

- Germany

- Market Size & Forecast, By Product & Service, (USD Million)

- Market Size & Forecast, By Technology (USD Million)

- Market Size & Forecast, By Application (USD Million)

- Market Size & Forecast, By End User (USD Million)

- France

- Market Size & Forecast, By Product & Service, (USD Million)

- Market Size & Forecast, By Technology (USD Million)

- Market Size & Forecast, By Application (USD Million)

- Market Size & Forecast, By End User (USD Million)

- Italy

- Market Size & Forecast, By Product & Service, (USD Million)

- Market Size & Forecast, By Technology (USD Million)

- Market Size & Forecast, By Application (USD Million)

- Market Size & Forecast, By End User (USD Million)

- Spain

- Market Size & Forecast, By Product & Service, (USD Million)

- Market Size & Forecast, By Technology (USD Million)

- Market Size & Forecast, By Application (USD Million)

- Market Size & Forecast, By End User (USD Million)

- Rest of Europe

- Market Size & Forecast, By Product & Service, (USD Million)

- Market Size & Forecast, By Technology (USD Million)

- Market Size & Forecast, By Application (USD Million)

- Market Size & Forecast, By End User (USD Million)

- Asia Pacific (APAC) Digital Health Market Size & Forecast (2022-2029), By Country, USD Million

- China

- Market Size & Forecast, By Product & Service, (USD Million)

- Market Size & Forecast, By Technology (USD Million)

- Market Size & Forecast, By Application (USD Million)

- Market Size & Forecast, By End User (USD Million)

- Japan

- Market Size & Forecast, By Product & Service, (USD Million)

- Market Size & Forecast, By Technology (USD Million)

- Market Size & Forecast, By Application (USD Million)

- Market Size & Forecast, By End User (USD Million)

- India

- Market Size & Forecast, By Product & Service, (USD Million)

- Market Size & Forecast, By Technology (USD Million)

- Market Size & Forecast, By Application (USD Million)

- Market Size & Forecast, By End User (USD Million)

- Rest of Asia Pacific

- Market Size & Forecast, By Product & Service, (USD Million)

- Market Size & Forecast, By Technology (USD Million)

- Market Size & Forecast, By Application (USD Million)

- Market Size & Forecast, By End User (USD Million)

- Latin America (LATAM) Digital Health Market Size & Forecast (2022-2029), USD Million

- Market Size & Forecast, By Product & Service, (USD Million)

- Market Size & Forecast, By Technology (USD Million)

- Market Size & Forecast, By Application (USD Million)

- Market Size & Forecast, By End User (USD Million)

- Middle East & Africa (MEA) Digital Health Market Size & Forecast (2022-2029), USD Million

- Market Size & Forecast, By Product & Service, (USD Million)

- Market Size & Forecast, By Technology (USD Million)

- Market Size & Forecast, By Application (USD Million)

- Market Size & Forecast, By End User (USD Million)

- China

- UK

- US

- Competitive Landscape

- Key Players and their Competitive Positioning

- Key Player Comparison

- Segment-wise Player Mapping

- Market Share Analysis (2023)

- Company Categorization Matrix

- Dominants/Leaders

- New Entrants

- Emerging Players

- Innovative Players

- Key Strategies Assessment, By Player (2022-2024)

- New Product Launches

- Partnerships, Agreements, & Collaborations

- Mergers & Acquisitions

- Geographic Expansion

- Key Players and their Competitive Positioning

- Company Profiles*

(Business Overview, Financial Performance**, Products Offered, Recent Developments)

- Koninklijke Philips N.V.

- Medtronic plc

- GE HealthCare

- OMRON Corporation

- Google, Inc.

- Johnson & Johnson Services, Inc.

- Siemens Healthineers AG

- Apple Inc.

- Veradigm LLC

- athenahealth

- Other Prominent Players

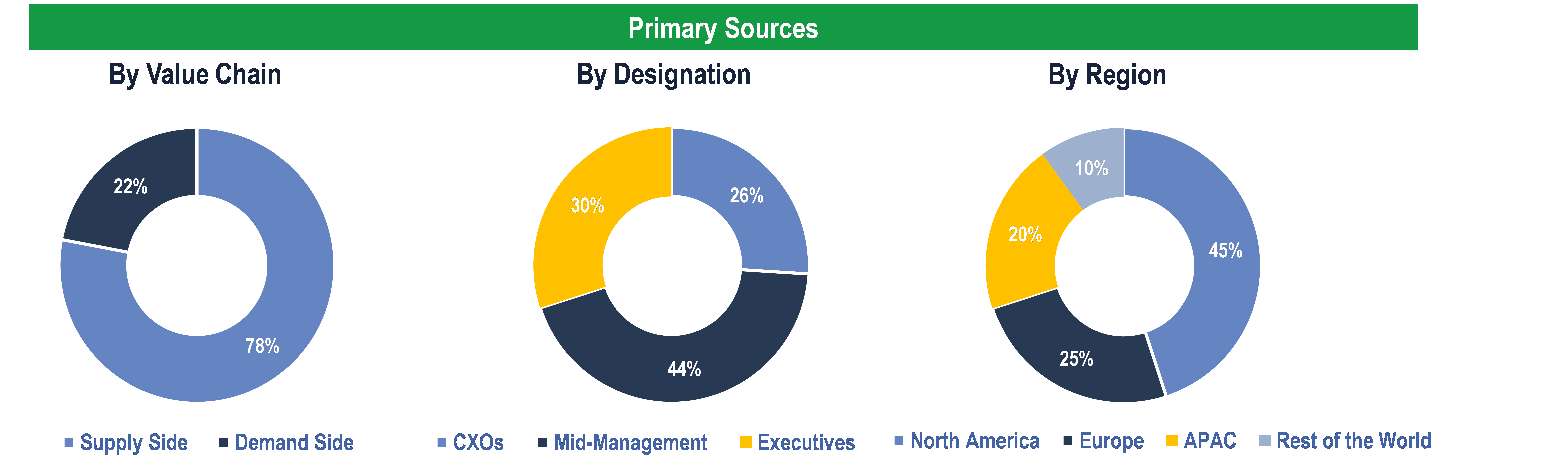

The study has been compiled based on extensive primary and secondary research.

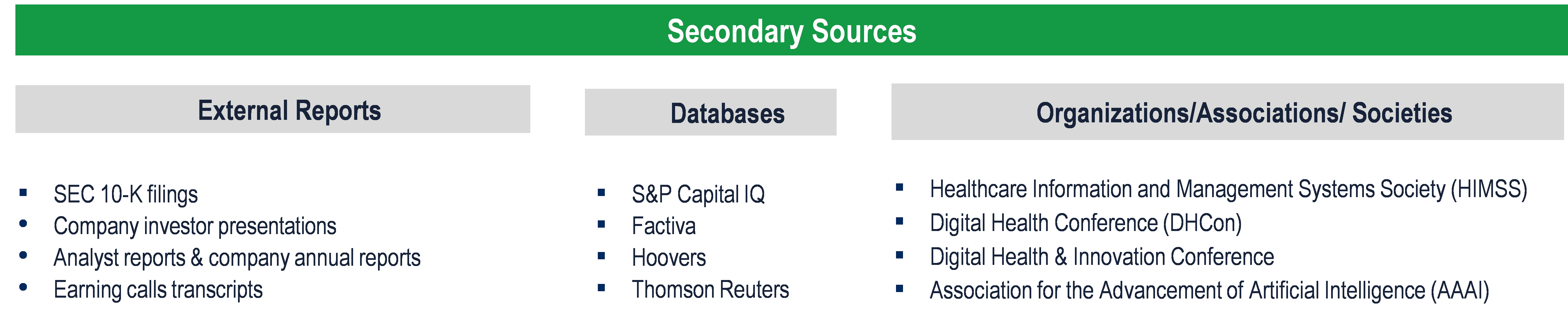

Secondary Research (Indicative List)

Primary Research

To validate research findings (market size & forecasts, market segmentation, market dynamics, competitive landscape, key industry trends, etc.), extensive primary interviews were conducted with both supply and demand-side stakeholders.

Supply Side Stakeholders:

- Senior Management Level: CEOs, Presidents, Vice-Presidents, Directors, Chief Technology Officers, Chief Commercial Officers

- Mid-Management Level: Product Managers, Sales Managers, Brand Managers, R&D Managers, Business Development Managers, Consultants

Demand Side Stakeholders:

- Hospitals & Clinics, Long Term Care Facilities, Assisted Living Centers, Payers, and others

Breakdown of Primary Interviews

Market Size Estimation

Both ‘Top-Down & Bottom-Up Approaches’ were used to derive market size estimates and forecasts

Data Triangulation

Research findings derived through secondary sources & internal analysis was validated with Primary Interviews, Internal Knowledge Repository and Company’s Sales Data