Urology and Pelvic Health Market – Growing Cases of Bladder Cancer & Kidney Stones

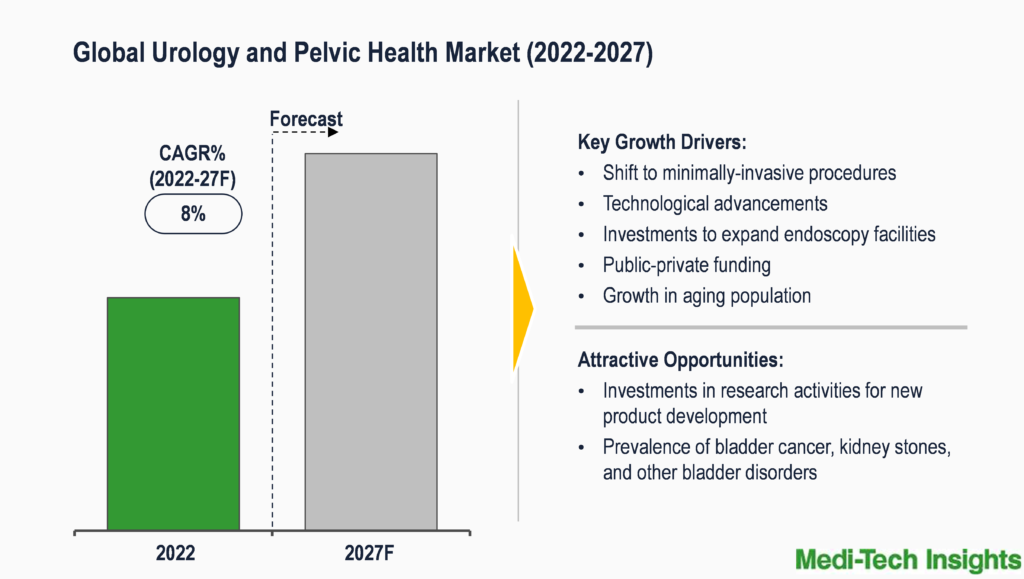

The global urology and pelvic health market is set to witness a growth rate of 8% in the next 5 years. Shift to minimally-invasive procedures; increasing prevalence of bladder cancer, kidney stones, and other bladder disorders; technological advancements in urology and pelvic health devices; and investments in research activities for new product development by leading market players are some of the key factors driving the market growth.

Urology and pelvic health is a medical and surgical specialty involving disorders of the genitourinary tract and the adrenal glands. Urologists addresses the conditions affecting kidneys, ureters, bladder, and urethra in both men and women. The urology and pelvic health market is segmented on the basis of product, application, and end-user.

Technological Advancements in Urology And Pelvic Health Market to fuel its Global Market Demand

Continuous advancements in urology and pelvic health market have enabled to develop efficient products with advanced capabilities such as minimally invasive approach, rapid recovery, and reduced infections. Major players have recently launched technologically advanced products to expand their geographic and strengthen their position in the global urology and pelvic health market. Some of the technological advancements are listed below:

- In November 2022, Teleflex launched its UroLift System in India, a minimally invasive approach for the treatment of benign prostatic hyperplasia (BPH) or prostate enlargement providing a rapid symptomatic relief for men allowing quick recovery.

- In November 2022, Coloplast launched SpeediCath Flex Set, a new catheter in the US market, featuring a triple action coating technology specifically designed to reduce the risk of Urinary Tract Infections (UTIs) and urethral damage.

- In September 2022, Olympus Corporation launched its VISERA ELITE III Surgical Visualization Platform that support imaging functions and minimally invasive therapies, to address the needs of healthcare professionals for endoscopic procedures including urology.

- In May 2022, Auris Health, Inc., a subsidiary of Ethicon, Inc., received the 510(k) clearance from the U.S. Food and Drug Administration (FDA) for its MONARCH Platform for endourological procedures.

In November 2021, The Flume Catheter Company Ltd. (TFCC) received the US Food and Drug Administration (FDA) clearance for its FLUME catheter, a new indwelling urinary catheter designed to address the drawbacks of traditional Foley catheter design.

Investments by Leading Market Players in Urology And Pelvic Health Market to drive the Product Development

Market players operating in the urology and pelvic health market are constantly focusing on investments and collaborations for advancing new product developments. These investments are targeted at boosting the technological capability of companies aiming at new product developments that offers significant gains to the company and its end users. Such advancements tend to provide a competitive edge to all the manufacturers. Some of the recent developments are listed below-

- In December 2022, Minze Health, a Belgium-based digital health company raised US$ 4.2 million (€ 3.9 million) from White Fund, Capricorn Partners, and PMV; to further scale its digital health solutions aimed at treating urinary tract problems.

- In April 2022, Cosm, a Canada-based start-up raised US$ 3.8 million (CAD 4.7 million) to advance its digital gynecology platform, a software-enabled medical device platform aimed at treating pelvic floor disorders.

- In September 2021, Boston Scientific Corporation acquired the global surgical business of Lumenis LTD. This acquisition was aimed at integrating the Lumenis laser portfolio with Boston Scientific’s kidney stone management and benign prostatic hyperplasia offerings.

- In April 2021, Renovia, a digital therapeutics company raised US$ 17 million Series C-1 financing round backed by Perceptive Life Sciences, Longwood Fund, Ascension Ventures and OSF Ventures, and Parian Global Management; to support the clinical development and launch of leva digital therapeutic used for the treatment of urinary incontinence and other pelvic floor disorders.

North America is expected to hold a major share in the Urology And Pelvic Health Market

From a geographical perspective, North America holds a major market share of the urology and pelvic health market. This can be mainly attributed to the investments by hospitals to procure advanced urology and pelvic health devices, favorable reimbursement policies, and developed healthcare infrastructure.

For instance, in December 2021, Vizient Inc. (a US-based member-owned healthcare company which includes academic medical centers, pediatric facilities, community hospitals, integrated health delivery networks and non-acute health care providers) and Ambu Inc. (manufacturer of single-use endoscopes) entered in a contract to offer Vizient members a pre-negotiated pricing for Ambu’s single-use products in bronchoscopy, urology, ENT and GI.

However, the Asia Pacific is expected to ascend at the fastest CAGR over the forecast period on account of the large customer base and growing health concerns in key markets such as Japan, China & India; rising disposable income; improving healthcare infrastructure; and rapidly growing target patient population.

Competitive Landscape Analysis: Urology And Pelvic Health Market

The global urology and pelvic health market is marked by the presence of key market players such as follows:-

- Boston Scientific Corporation (US)

- Medtronic plc (Ireland)

- Coloplast (Denmark)

- B. Braun Melsungen AG (Germany)

- ConvaTec Group (UK)

- Hollister Incorporated (US)

- Teleflex Inc. (US)

- Stryker Corporation (US)

- Ethicon (US)

COVID-19 negatively impacted the Global Urology And Pelvic Health Market

The COVID-19 pandemic had a negative impact on some of the urology and pelvic health market players. Sales of these products fell significantly as a result of cancellations of non-urgent urological procedures. Some of the manufacturers reported significant revenue losses as a result of the fall in demand. However, post-pandemic, the demand is being supported by relaxation of restrictions, resumption of hospital services, and the steady increase in patient traffic. Company revenues have increased significantly since the pandemic.

Some of the restraints to market growth include high cost of advanced urology and pelvic health devices, unfavorable reimbursement scenario, and lack of experienced technicians. Irrespective of these issues, the urology and pelvic health market is expected to grow at a steady rate due to increased focus of market players on new product development with advanced capabilities. Substantial advancements in terms of minimally-invasive approach, reduction in subsequent infections, and high incidence of kidney diseases, among others, are expected to further drive the global urology and pelvic health market growth.

Key Strategic Questions Addressed in this Report

- What is the market size & forecast of the urology and pelvic health market?

- What are historical, present, and forecasted market shares and growth rates of various segments and sub-segments of the urology and pelvic health market?

- What are the key trends defining the urology and pelvic health market?

- What are the major factors impacting the urology and pelvic health market?

- What are the opportunities prevailing in the urology and pelvic health market?

- Which region has the highest share in the global market? Which region is expected to witness the highest growth rate in the next 5 years?

- Who are the major players operating in the urology and pelvic health market?

- What are the key strategies adopted by players operating in urology and pelvic health market?

1. Research Methodology

1.1. Secondary Research

1.2. Primary Research

1.3. Market Estimation

1.4. Market Forecasting

2. Executive Summary

3. Market Overview

3.1. Market Dynamics

3.1.1. Drivers

3.1.2. Restraints

3.1.3. Opportunities

3.1.4. Market Trends

3.2. Industry Speaks

3.3. Pricing Analysis (2020-2022)

3.4. Reimbursement Assessment (Key Markets)

4. COVID-19 Impact on Urology and Pelvic Health Market

5. Looming Recession (2023) – Key Challenges & Impact

6. Global Urology and Pelvic Health Market- Size & Forecast (2019-2027), By Product

6.1. Urinary Catheters

6.2. Urinary Incontinence Devices

6.3. Stone Management Devices

6.4. Benign Prostate Hyperplasia (BPH) Treatment Devices

6.5. Urological Endoscopes

6.6. Low Dose Radiation Brachytherapy (LDRB) Seeds

6.7. Erectile Dysfunction Devices

6.8. Urinary Guidewires

7. Global Urology and Pelvic Health Market- Size & Forecast (2019-2027), By Application

7.1. Kidney Disease

7.2. Urological Cancer & BPH

7.3. Pelvic Organ Prolapse

7.4. Other Applications

8. Global Urology and Pelvic Health Market- Size & Forecast (2019-2027), By End-User

8.1. Hospitals and Clinics

8.2. Ambulatory Surgical Centers (ASCs)

8.3. Home Care Settings

9. Global Urology and Pelvic Health Market- Size & Forecast (2019-2027), By Region

9.1. North America (U.S. & Canada)

9.2. Europe (UK, Germany, France, Italy, Spain, Rest of Europe)

9.3. Asia Pacific (China, India, Japan, Rest of Asia Pacific)

9.4. Rest of the World (Latin America, Middle East & Africa)

10. Competitive Landscape

10.1. Key Players and their Competitive Positioning

10.1.1. Market Share Analysis (2022)

10.1.2. Segment-wise Player Mapping

10.2. Key Strategies Assessment, By Player (2020-2022)

10.2.1. New Product & Service Launches

10.2.2. Partnerships, Agreements, & Collaborations

10.2.3. Mergers & Acquisitions

10.2.4. Geographic Expansion

11. Key Companies Scanned (Indicative List)

11.1. Boston Scientific Corporation

11.2. Medtronic plc

11.3. Coloplast

11.4. B. Braun Melsungen AG

11.5. ConvaTec Group

11.6. Hollister Incorporated

11.7. Teleflex Inc.

11.8. Stryker Corporation

11.9. Ethicon

11.10. Olympus Corporation

The study has been compiled based on the extensive primary and secondary research.

Secondary Research (Indicative List)

Primary Research

To validate research findings (market size & forecasts, market segmentation, market dynamics, competitive landscape, key industry trends, etc.), extensive primary interviews were conducted with both supply and demand side stakeholders.

Supply Side Stakeholders:

- Senior Management Level: CEOs, Presidents, Vice-Presidents, Directors, Chief Technology Officers, Chief Commercial Officers

- Mid-Management Level: Product Managers, Sales Managers, Brand Managers, R&D Managers, Business Development Managers, Consultants

Demand Side Stakeholders:

- Stakeholders in Public and Private Hospitals, Clinics, and Ambulatory Surgical Centers.

Breakdown of Primary Interviews

Market Size Estimation

Both ‘Top-Down and Bottom-Up Approaches’ were used to derive market size estimates and forecasts.

Data Triangulation

Research findings derived through secondary sources & internal analysis were validated with Primary Interviews, Internal Knowledge Repository, and Company Sales Data.