Global Minimally Invasive Orthopedic Procedures Market Size: Segmented by Product (Surgical Instruments, Implants, Equipment, Consumables/Accessories), Procedure (Joint Replacement, Arthroscopic, Spine), Technology (Robotic, Computer-assisted), End User Analysis & Regional Forecast to 2031

The global minimally invasive orthopedic procedures market size is set to witness a growth rate of 9% in the next 5 years. Rising burden of orthopedic disorders, benefits of minimally invasive orthopedic procedures, technological advancements, and shift toward outpatient and ASC settings are some of the key factors driving the minimally invasive orthopedic procedures market. To learn more about the research report, download a sample report.

Minimally invasive orthopedic procedure refers to advanced surgical techniques for diagnosing and treating musculoskeletal problems by using very small incisions. Minimally invasive orthopedic procedures use specialized instruments, arthroscopes, endoscopes, robot-assisted systems, and computer- guided navigation to allow the surgeon to be more accurate and to minimize trauma to the body during the surgical process. Some common examples of minimally invasive orthopedic procedures include joint replacement, spine surgery, fracture fixation, and repairs of sports-related injuries. In comparison to traditional open surgery, minimally invasive orthopedic procedures usually result in less blood loss, decreased risk of infection, shorter hospital stays, less postoperative pain, and faster rehabilitation time, thereby making them much less appealing for both surgeons and patients because of superior clinical outcomes and much quicker return to normal activity following surgery.

Rising burden of orthopedic disorders to propel market demand

One major factor driving the expansion of the minimally invasive orthopedic procedure market has been the increasing incidence of orthopedic disorders worldwide. Musculoskeletal disorders like osteoarthritis, rheumatoid arthritis, degenerative disc disease, osteoporosis, and traumatic fractures are all becoming more prevalent worldwide. Global cases of musculoskeletal disorders rose from 221 million in 1990 to 494 million in 2020 (up 123%) and are projected to reach approximately 1.06 billion by 2050, reflecting continued rapid growth (Source: WHO). Many aging adults with lower bone density, damaged cartilage, and accelerated joint degeneration due to normal aging will likely need surgical interventions including joint replacements, spine stabilizations, and fracture fixations.

The orthopedic disease burden is also being impacted by changing lifestyle patterns. Sedentary behavior, obesity, poor posture, and lack of physical activity contribute to joint stress and spinal disorders. At the same time, increasing participation in sports and fitness activities has led to a higher incidence of ligament tears, meniscal injuries, rotator cuff injuries, and other sports-related trauma. Road accidents and workplace injuries also add to the growing number of trauma cases requiring surgical management.

An increase in orthopedic procedures has placed a strain on healthcare facilities to provide effective care while optimizing their use of hospital resources and lowering the cost of care. A viable option for providing effective treatment in an increasingly cost-conscious environment is through utilizing minimally invasive techniques as an alternative to traditional open surgery methods. These types of procedures involve smaller incisions, disrupts less soft tissue, have a lower blood loss, and ultimately result in shorter hospitalizations than traditional techniques. As a result of these innovative advantages, patients can expect to recover from surgery more quickly, have fewer complications, and have higher levels of satisfaction with their outcomes. Further, for geriatric patients, the minimization of trauma due to surgery helps to decrease the likelihood of postoperative complications and expedite the rehabilitation process.

The increase in the incidence of disease means that the number of procedures performed each year, including those involving joint replacements, spine surgery, and arthroscopy, is also increasing, and as surgeons become more familiar with minimally invasive techniques, their application is expected to become more common across all classifications of surgeries. In addition to being an attractive option for patients, both hospitals and outpatient or surgical centers view minimally invasive procedures to improve the flow of patients through their facility and to reduce the length of stay for patients in the hospital.

Overall, as the incidence of orthopaedic-related disease continues to increase, this leads to a corresponding increase in the number of potential patients eligible for surgical intervention, and the numerous advantages associated with minimally invasive techniques will make them the preferred surgical technique for the increasing number of patients receiving orthopaedic surgeries. This is expected to create an ever-increasing growth trend globally for minimally invasive surgical techniques.

To learn more about this report, download the PDF brochure

Shift toward outpatient and ASC settings is driving the market growth

There is a strong trend towards providing outpatient and ASCs, which is fueling growth in the market for minimally invasive orthopedic procedures. Health care systems globally are trying to be more cost-efficient, lessen the burden of hospitals and make it easier for their patients to access care. Minimally invasive orthopedic techniques are a good fit for these goals because of the smaller size of the incisions used, the lower amount of trauma caused to surrounding soft tissue, less blood loss, and faster recovery times associated with these procedures. Due of these traits, many orthopedic surgeries are amenable to outpatient discharge on the same day they are performed, moving many of these surgeries from the more traditional inpatient hospital setting into outpatient facilities.

ASCs provide a more efficient model for delivering health care. The number of Medicare-Certified ASCs in the US increased from 5927 in 2020 to 6394 in 2024 (Source: Ambulatory Surgery Center Association). The ASC space is expanding as procedures move out of traditional hospitals due to benefits in lower cost, flexible timing, and personalized care. ASCs typically have lower overhead costs, shorter scheduling times, and more predictable workflow than hospitals. For payers and providers, this means decreased cost for procedures and more effective use of resources. As reimbursement models shift to value-based care, providers will be incentivized to complete procedures in lower-cost settings without sacrificing quality. Minimally invasive orthopedic procedures, such as arthroscopic surgery, minimally invasive spinal procedures, and some joint replacement procedures, are increasingly being done in ASCs since they have good safety and recovery profiles.

Another key driver of this transition is patient preference. Many patients would rather have outpatient procedures done due to their reduced time spent in a hospital, less chance of patient-to-patient spread of hospital-acquired diseases, and more chance to recover in their own home. Patients also support same-day discharge protocols because they can be mobilized faster following Outpatient surgical procedures and experience less pain than they usually do postoperatively. Enhanced techniques of anesthesia delivery improved postoperative pain management processes, superior imaging equipment and robotic-assisted systems all provide surgical precision, improve confidence in performing numerous complex orthopedic procedures outside of the traditional inpatient environment, and lower the risk of complication.

As orthopedic procedures continue to migrate to ASCs, there is an increased requirement for use of minimally invasive instruments, implants, navigation systems and robotic platforms. Healthcare providers are investing money into purchasing equipment specifically designed to facilitate outpatient workflows. The overall structural transition toward outpatient and ASC environments also creates a continuing increase in the number and types of procedures, improved access to and use of minimally invasive orthopedic procedures, and thus, continuing growth of the orthopedic market.

Growth strategies adopted by players to establish their foothold in the market

Players operating in this market are adopting various growth strategies such as new product launches and approvals, strategic partnerships and collaborations, and acquisitions to garner market share. For instance,

- In January 2026, Smith+Nephew completed the acquisition of Integrity Orthopaedics, adding the Tendon Seam system to strengthen its rotator cuff repair portfolio. The innovative biomechanical repair technology, cleared in 2023, is designed to reduce re-tear rates and improve outcomes, complementing Smith+Nephew’s REGENETEN implant in the growing US sports medicine market

- In September 2025, Arthrex launched the NanoNeedle Scope 2.0, a third generation minimally invasive imaging platform featuring a 720×720 sensor with 224% higher resolution. The device received FDA clearance for paediatric orthopaedics under the Synergy Vision system and is positioned as a potential gold standard for ultra-minimally invasive paediatric arthroscopy

- In April 2025, Point Robotics MedTech Inc. partnered with CTL Amedica (CTLA) to expand the minimally invasive spinal navigation market across the Americas. The agreement enables CTLA to distribute Point Robotics’ navigation systems in the region, combining advanced navigation technology with an established implant network to deliver cost-effective orthopedic solutions

- In October 2023, DePuy Synthes (part of Johnson & Johnson MedTech), officially launched the VELYS Robotic-Assisted Solution in Europe, with successful total knee surgeries performed in Germany, Belgium, and Switzerland. The imageless, table-mounted robotic system integrates with the ATTUNE Knee System, enhances surgical precision and efficiency without requiring pre-operative CT scans, and supports improved patient outcomes in total knee arthroplasty

- In September 2023, Stryker Corporation launched PROstep MIS Lapidus, a minimally invasive internal fixation system for bunion correction, debuting at the American Orthopaedic Foot & Ankle Society Annual Meeting. The system offers improved fixation stability with smaller incisions, demonstrating reduced recurrence, lower non-union rates, significantly smaller scars, and decreased post-operative opioid use compared to traditional open Lapidus procedures

To learn more about this report, download the PDF brochure

Procedure Segment Outlook

Joint replacement represents the largest segment in the minimally invasive orthopedic procedures market. This is due partly by high volumes of hip and knee arthroplasties happening worldwide, particularly among older adults with osteoarthritis & degenerative joint diseases. In addition, patients are preferring minimally invasively methods to have their total knee and hip replaced as it leads to a faster recovery time and shorter hospital stays. Spine surgery, however, is the fastest growing segment primarily due to the increasing occurrence of degenerative disc disease, advanced technology for navigation and robotics, and the overall adoption of minimally invasive techniques that reduce complication and accelerate rehabilitation for patients.

Regional Outlook: North America expected to hold a major share in the minimally invasive orthopedic procedures market

With high-volume surgical activity, advanced medical facilities, a strong reimbursement system and fast-growing robotics & navigation technologies, represents the largest regional segment in the minimally invasive orthopedic procedures market. The presence of leading orthopedic product suppliers and an early adoption of new MIS techniques further adds to North America's higher share in the global MIS orthopedic market. Asia Pacific is the fastest-growing region within the MIS orthopedic global market, with growing access to healthcare facilities and advances in medical tourism, a rapidly growing aging population, rapidly growing incidence of musculoskeletal disorders, and improving access to advanced surgical instruments & processes in China, India, and Japan.

Competitive Landscape Analysis

The global minimally invasive orthopedic procedures market is marked by the presence of established and emerging market players such as Intuitive Surgical Operations, Inc. (US); Medtronic (Ireland); Johnson & Johnson (US); Stryker Corporation (US); Zimmer Biomet (US); Smith+Nephew (UK); KARL STORZ (Germany); Boston Scientific Corporation (US); Globus Medical (US); and CONMED Corporation (US); among others. Some of the key strategies adopted by market players include new product launches and approvals, strategic partnerships and collaborations, and acquisitions.

Get a sample report for competitive landscape analysis

Report Scope

|

Report Metric |

Details |

|

Base Year Considered |

2025 |

|

Historical Data |

2024 – 2025 |

|

Forecast Period |

2026 – 2031 |

|

Growth Rate |

9% |

|

Segment Scope |

Product, Procedure, Technology, End User |

|

Regional Scope |

|

|

Market Drivers |

|

|

Attractive Opportunities |

|

|

Key Companies Mapped |

Intuitive Surgical Operations, Inc. (US); Medtronic (Ireland); Johnson & Johnson (US); Stryker Corporation (US); Zimmer Biomet (US); Smith+Nephew (UK); KARL STORZ (Germany); Boston Scientific Corporation (US); Globus Medical (US); and CONMED Corporation (US); among others |

|

Report Highlights |

Market Size & Forecast, Growth Drivers & Restraints, Trends, Competitive Analysis |

Global Minimally Invasive Orthopedic Procedures Market Segmentation

This report by Medi-Tech Insights provides the size of the global minimally invasive orthopedic procedures market at the regional- and country-level from 2024 to 2031. The report further segments the market based on product, procedure, technology, application, and end user.

Market Size & Forecast (2024-2031), By Product, USD Billion

- Arthroscopy Systems

- Endoscopic Surgery Systems

Market Size & Forecast (2024-2031), By Procedure, USD Billion

- Joint Replacement

- Spine Surgery

- Trauma and Fracture Fixation

- Sports Medicine Procedures

- Other Procedures

Market Size & Forecast (2024-2031), By Technology, USD Billion

- Robotic-assisted Systems

- Computer-assisted Navigation Systems

- Other Technologies

Market Size & Forecast (2024-2031), By End User, USD Billion

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Specialty Orthopedic Clinics

- Other End Users

Market Size & Forecast (2024-2031), By Region, USD Billion

- North America

- US

- Canada

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Middle East & Africa

Related Reports

- Introduction

- Introduction

- Market Scope

- Market Definition

- Segments Covered

- Regional Segmentation

- Research Timeframe

- Currency Considered

- Study Limitations

- Stakeholders

- List of Abbreviations

- Key Conferences and Events (2026-2027)

- Research Methodology

- Secondary Research

- Primary Research

- Market Estimation

- Bottom-Up Approach

- Top-Down Approach

- Market Forecasting

- Executive Summary

- Minimally Invasive Orthopedic Procedures Market Snapshot (2026-2031)

- Segment Overview

- Regional Snapshot

- Competitive Insights

- Market Overview

- Market Dynamics

- Drivers

- Rising burden of orthopedic disorders

- Benefits of minimally invasive orthopedic procedures

- Technological advancements

- Shift toward outpatient and ASC settings

- Restraints

- High cost of advanced equipment

- Limited reimbursement and insurance coverage

- Shortage of skilled surgeons

- Regulatory and approval barriers

- Opportunities

- Growth in emerging healthcare markets

- Robotic-assisted orthopedic surgery

- Regenerative medicine and biologics

- Healthcare policy and geriatric focus

- Key Market Trends

- AI integration and digital surgical platforms

- Enhanced visualization and imaging

- Unmet Market Needs

- Industry Speaks

- Drivers

- Market Dynamics

- Global Minimally Invasive Orthopedic Procedures Market Size & Forecast (2024-2031), By Product, USD Billion

- Introduction

- Arthroscopy Systems

- Endoscopic Surgery Systems

- Global Minimally Invasive Orthopedic Procedures Market Size & Forecast (2024-2031), By Procedure, USD Billion

- Introduction

- Joint Replacement

- Spine Surgery

- Trauma and Fracture Fixation

- Sports Medicine Procedures

- Other Procedures

- Global Minimally Invasive Orthopedic Procedures Market Size & Forecast (2024-2031), By Technology, USD Billion

- Introduction

- Robotic-assisted Systems

- Computer-assisted Navigation Systems

- Other Technologies

- Global Minimally Invasive Orthopedic Procedures Market Size & Forecast (2024-2031), By End User, USD Billion

- Introduction

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Specialty Orthopedic Clinics

- Other End Users

- Global Minimally Invasive Orthopedic Procedures Market Size & Forecast (2024-2031), By Region, USD Billion

- Introduction

- North America Minimally Invasive Orthopedic Procedures Market Size & Forecast (2024-2031), By Country, USD Billion

- US

- Market Size & Forecast, By Product, (USD Billion)

- Market Size & Forecast, By Procedure (USD Billion)

- Market Size & Forecast, By Technology (USD Billion)

- Market Size & Forecast, By End User (USD Billion)

- Canada

- Market Size & Forecast, By Product, (USD Billion)

- Market Size & Forecast, By Procedure (USD Billion)

- Market Size & Forecast, By Technology (USD Billion)

- Market Size & Forecast, By End User (USD Billion)

- US

- Europe Minimally Invasive Orthopedic Procedures Market Size & Forecast (2024-2031), By Country, USD Billion

- UK

- Market Size & Forecast, By Product, (USD Billion)

- Market Size & Forecast, By Procedure (USD Billion)

- Market Size & Forecast, By Technology (USD Billion)

- Market Size & Forecast, By End User (USD Billion)

- Germany

- Market Size & Forecast, By Product, (USD Billion)

- Market Size & Forecast, By Procedure (USD Billion)

- Market Size & Forecast, By Technology (USD Billion)

- Market Size & Forecast, By End User (USD Billion)

- France

- Market Size & Forecast, By Product, (USD Billion)

- Market Size & Forecast, By Procedure (USD Billion)

- Market Size & Forecast, By Technology (USD Billion)

- Market Size & Forecast, By End User (USD Billion)

- Italy

- Market Size & Forecast, By Product, (USD Billion)

- Market Size & Forecast, By Procedure (USD Billion)

- Market Size & Forecast, By Technology (USD Billion)

- Market Size & Forecast, By End User (USD Billion)

- Spain

- Market Size & Forecast, By Product, (USD Billion)

- Market Size & Forecast, By Procedure (USD Billion)

- Market Size & Forecast, By Technology (USD Billion)

- Market Size & Forecast, By End User (USD Billion)

- Rest of Europe

- Market Size & Forecast, By Product, (USD Billion)

- Market Size & Forecast, By Procedure (USD Billion)

- Market Size & Forecast, By Technology (USD Billion)

- Market Size & Forecast, By End User (USD Billion)

- UK

- Asia Pacific (APAC) Minimally Invasive Orthopedic Procedures Market Size & Forecast (2024-2031), By Country, USD Billion

- China

- Market Size & Forecast, By Product, (USD Billion)

- Market Size & Forecast, By Procedure (USD Billion)

- Market Size & Forecast, By Technology (USD Billion)

- Market Size & Forecast, By End User (USD Billion)

- Japan

- Market Size & Forecast, By Product, (USD Billion)

- Market Size & Forecast, By Procedure (USD Billion)

- Market Size & Forecast, By Technology (USD Billion)

- Market Size & Forecast, By End User (USD Billion)

- India

- Market Size & Forecast, By Product, (USD Billion)

- Market Size & Forecast, By Procedure (USD Billion)

- Market Size & Forecast, By Technology (USD Billion)

- Market Size & Forecast, By End User (USD Billion)

- Rest of Asia Pacific

- Market Size & Forecast, By Product, (USD Billion)

- Market Size & Forecast, By Procedure (USD Billion)

- Market Size & Forecast, By Technology (USD Billion)

- Market Size & Forecast, By End User (USD Billion)

- China

- Latin America (LATAM) Minimally Invasive Orthopedic Procedures Market Size & Forecast (2024-2031), USD Billion

- Market Size & Forecast, By Product, (USD Billion)

- Market Size & Forecast, By Procedure (USD Billion)

- Market Size & Forecast, By Technology (USD Billion)

- Market Size & Forecast, By End User (USD Billion)

- Middle East & Africa (MEA) Minimally Invasive Orthopedic Procedures Market Size & Forecast (2024-2031), USD Billion

- Market Size & Forecast, By Product, (USD Billion)

- Market Size & Forecast, By Procedure (USD Billion)

- Market Size & Forecast, By Technology (USD Billion)

- Market Size & Forecast, By End User (USD Billion)

- Competitive Landscape

- Key Players and their Competitive Positioning

- Key Player Comparison

- Segment-wise Player Mapping

- Market Share Analysis (2025)

- Company Categorization Matrix

- Dominants/Leaders

- New Entrants

- Emerging Players

- Innovative Players

- Key Strategies Assessment, By Player (2023-2026)

- New Product Launches

- Partnerships, Agreements, & Collaborations

- Mergers & Acquisitions

- Geographic Expansion

- Key Players and their Competitive Positioning

- Company Profiles*

(Business Overview, Financial Performance**, Products Offered, Recent Developments)

- Intuitive Surgical Operations, Inc.

- Medtronic

- Johnson & Johnson

- Stryker

- Zimmer Biomet

- Smith+Nephew

- KARL STORZ

- Boston Scientific Corporation

- Globus Medical

- CONMED Corporation

- Other Prominent Players

Note: *Indicative list

**For listed companies

The study has been compiled based on extensive primary and secondary research.

Secondary Research (Indicative List)

Primary Research

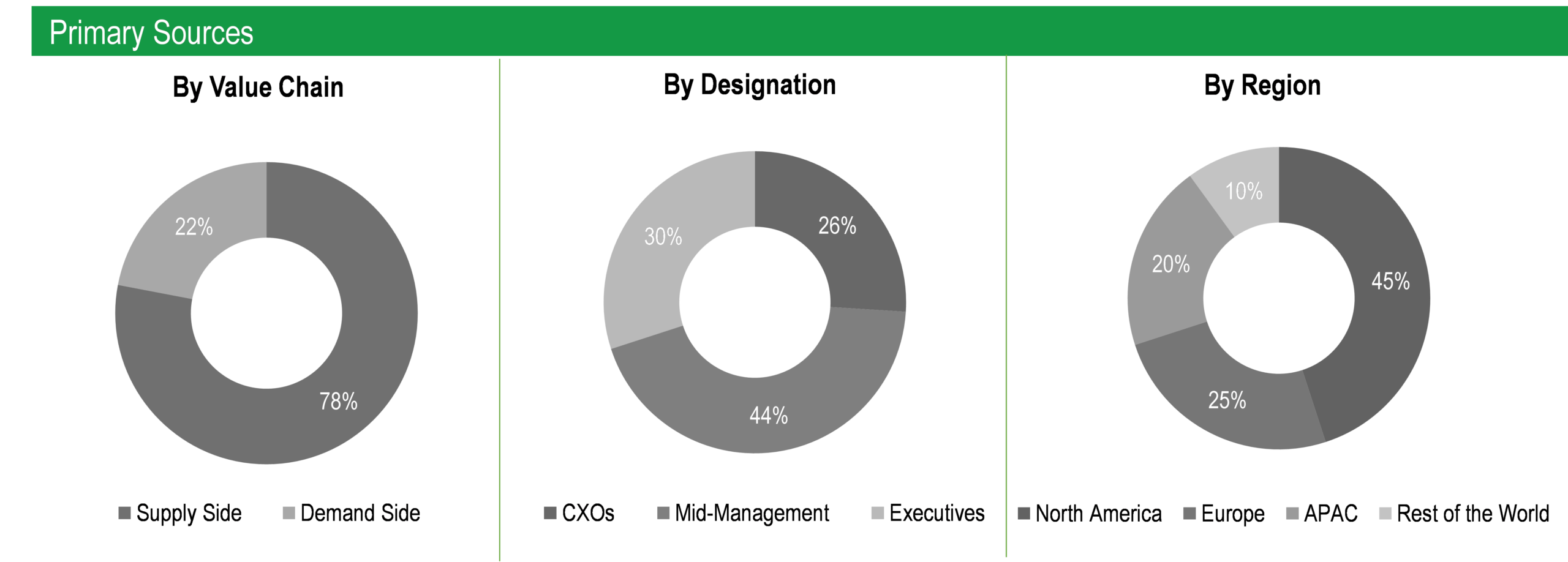

To validate research findings (market size & forecasts, market segmentation, market dynamics, competitive landscape, key industry trends, etc.), extensive primary interviews were conducted with both supply and demand-side stakeholders.

Supply Side Stakeholders:

- Senior Management Level: CEOs, Presidents, Vice-Presidents, Directors, Chief Technology Officers, Chief Commercial Officers

- Mid-Management Level: Product Managers, Sales Managers, Brand Managers, R&D Managers, Business Development Managers, Consultants

Demand Side Stakeholders:

- Hospitals and Clinics, Ambulatory Surgery Centers (ASCs), Specialty Orthopedic Clinics, and others

Breakdown of Primary Interviews

Market Size Estimation

Both ‘Top-Down & Bottom-Up Approaches’ were used to derive market size estimates and forecasts

Data Triangulation

Research findings derived through secondary sources & internal analysis was validated with Primary Interviews, Internal Knowledge Repository and Company’s Sales Data

Features of the Report

- Comprehensive Market Coverage

- Market Size and Forecast

- Geographic & Segment Deep Dives

- Strategic Insights & Competitive Landscape

- Timely & Updated Data

- Growth Indicators & Future Outlook

- Quick Turnaround on Queries

- Analyst Support

- Report Customization Available

- Reports in PDF & Excel